On December 19, 2018, Federal Reserve Chair Jerome Powell raised rates and described the balance sheet runoff as on "autopilot", signaling that the Fed would continue tightening regardless of market conditions. The S&P 500 sold off sharply, culminating in the worst Christmas Eve session on record. By December 24, the index had fallen approximately 20% from its September high.

The Fed reversed course within weeks.

What made this event analytically distinctive is that it was not a surprise. The narrative conditions for a policy error had been building for ten weeks. Perscient's semantic signatures captured that buildup across multiple timeframes, and with progressively sharper precision as the crisis approached.

The October 10–11 selloff — ten weeks before the Christmas Eve bottom — was significant not for its magnitude but for what it revealed about market psychology underneath.

During those two sessions, the Investors Are Panicking signature spiked to 4–7× its baseline level. That alone was not unusual; sharp corrections routinely produce panic readings. What was unusual was what happened next: the signature did not normalize.

Through November and into early December, Financial Advisor channel signatures measuring defensive positioning — including Time for Investors to Get Defensive (Z-score above +1.5) and HNW Investors Scared to Get Back In (persistently positive) — remained elevated long after prices had partially recovered. In a typical correction, sentiment normalizes as prices recover. Here it didn't. That persistence was a signal that the October shock had permanently reset investor psychology rather than temporarily disrupting it.

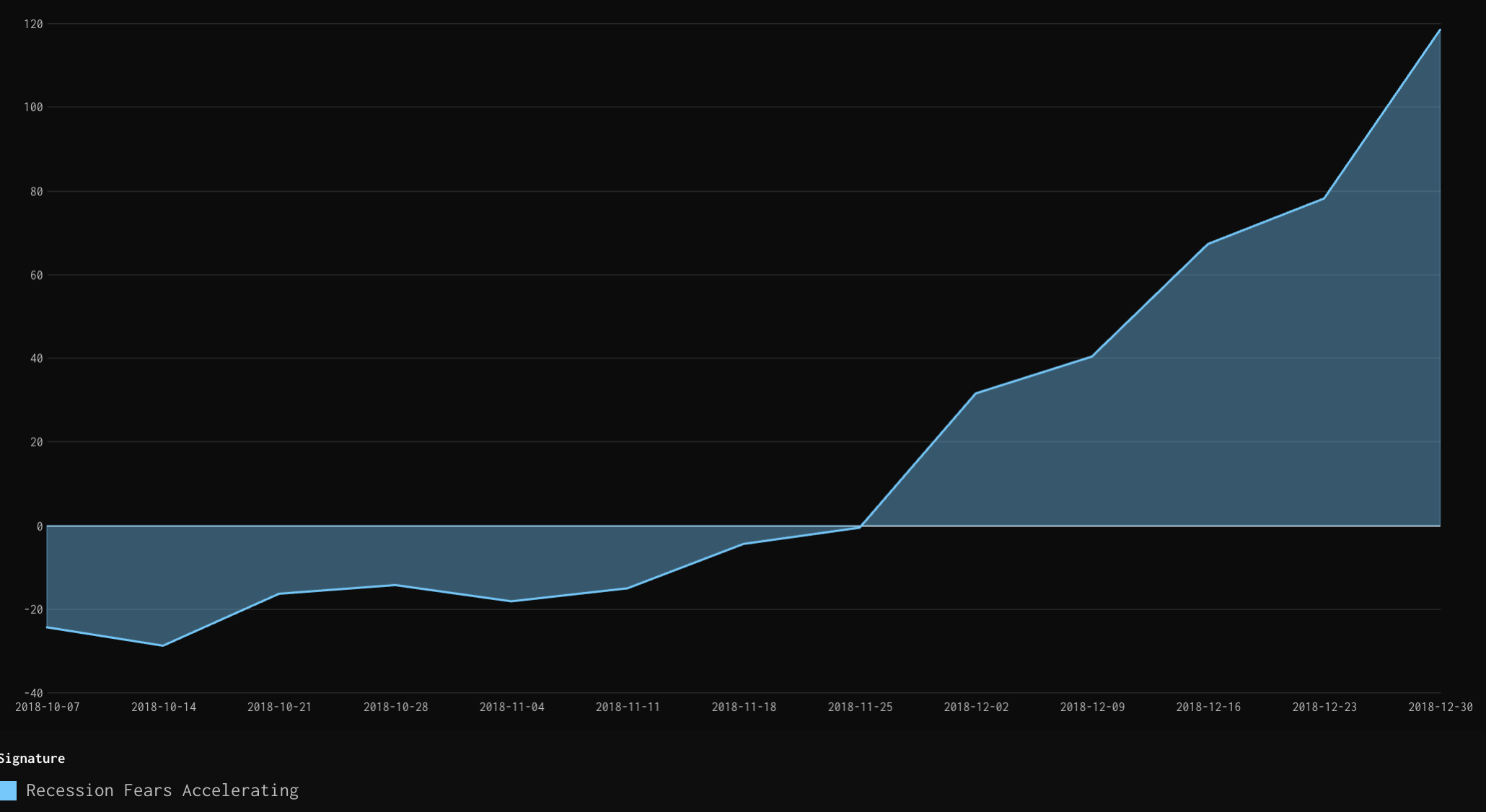

On December 4–5, 2018 — two full weeks before Powell's press conference — the Recession Fears Accelerating signature spiked to 117–119 on the index, its highest readingof the year.

This is the most important leading signal in the dataset.The recession narrative had reached a critical threshold before the Fed made any communication error. Markets were not reacting to Powell on December 19; they were confirming a narrative that had already turned. The policy mistake was the catalyst, not the cause.

For investors monitoring this signal in real time, the December 4–5 spike represented a meaningful warning: the market's underlying narrative had shifted to recession risk, and the Fed was walking into a meeting with a fragile consensus already in place.

The CB Doesn't Have Market's Back signature reached 176 on December 18 — one day beforePowell's press conference.

This is a precise leading signal. Market participants had pre-positioned for disappointment before Powell spoke. The narrative that the Fed would not act to support markets had already peaked at its highest point; what followed on December 19 was confirmation, not revelation. The signature was capturing the market's conviction that the Fed was about to disappoint —and it was right.

Taken together, these three signals created a mosaic with layered lead times: the systemic fragility warning (October, 75 days), the recession narrative shift (December 4–5, 20 days), and the Fed credibility erosion (December 18, 1 day). Each progressively narrowed the window, but each also sharpened the conviction.

The December 2018 case illustrates a recurring pattern in policy-driven crises: the narrative deteriorates well before the policy mistake occurs, and the narrative leads the market.

Three specific conditions were present and measurable in the signature data before Powell's press conference:

1. Embedded fear— investor psychology had not recovered from October, leaving the market structurally vulnerable

2. Recession narrative — the economic story had turned negative two weeks early, priming markets for disappointment

3. Anticipated Fed abandonment — the CB Doesn't Have Market's Back signature peaked one day before the event, capturing the market's conviction that the Fed would not actto support prices

None of this required predicting what Powell would say. The narrative conditions that made his words so damaging were already visible inthe data.

This is the core value proposition of semantic signature analysis for risk monitoring: policy-driven crises are not random shocks. They emerge from a building narrative environment that the signatures capture inreal time — at 75 days, at 20 days, and at 1 day — giving analysts and portfolio managers actionable lead time at each horizon.

Perscient narrative intelligence tracks semantic signatures across financial media, analyst research, and public discourse. Signature readings are normalized as Z-scores on a rolling 90-day basis unless otherwise noted.

This commentary is being provided to you as general information only and should not be taken as investment advice. The opinions expressed in these materials represent the personal views of the author(s). It is not investment research or a research recommendation, as it does not constitute substantive research or analysis. Any action that you take as a result of information contained in this document is ultimately your responsibility. Perscient will not accept liability for any loss or damage, including without limitation to any loss of profit, which may arise directly or indirectly from use of or reliance on such information. Consult your investment advisor before making any investment decisions. It must be noted that no one can accurately predict the future of the market with certainty or guarantee future investment performance. Past performance is not a guarantee of future results.

Statements in this communication are forward-looking statements.

The forward-looking statements and other views expressed herein are as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements, and there is no guarantee that any predictions will come to pass. The views expressed herein are subject to change at any time, due to numerous market and other factors. Perscient disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

This information is neither an offer to sell nor a solicitation of any offer to buy any securities.

This commentary has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. Perscient recommends that investors independently evaluate particular investments and strategies, and encourages investors to seek the advice of a financial advisor. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.